Source: CUtoday

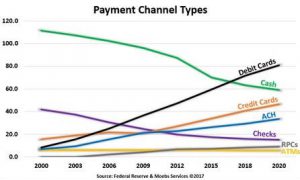

Did you know that debit card usage has surpassed coin and currency usage for the first time ever!? As we enter the third quarter of 2017, debit cards are reaching 66.3 billion transactions, while cash transactions total 65.9 billion transactions. While we don’t think any of our tried and true payment methods will be disappearing any time soon, it is important to recognize this shift in consumer habits and the impact that it has on credit unions. Never has it been more important to offer strong cards programs and to ensure members are making your card top of wallet.

Staying Top of Wallet

It used to be that when we referred to a “wallet,” we meant a physical, tangible billfold that was housed in a purse or pocket. Today, the term also can encompass mobile wallets, such as Apple Pay, Android Pay, or any apps that card information is pre-loaded into. But, once your members have loaded their mobile wallet, are they thinking about which card they use the most? It’s easy to discern cards in a physical wallet, but a mobile wallet can quickly become a “set-it-and-forget-it” matter.

“We continue to work closely with credit unions to develop strategies to not only become ‘top of wallet,’ but also to remain in this position as well,” shared Rebekah Higgins, Synergent’s Vice President of Payment Services. “Alternative payment methods are introduced to credit union cardholders on a regular basis; therefore, credit unions need to implement products and services that are valuable to their members and find ways to stay connected in the digital and virtual environments.”

Educating members about your credit union’s standard card features, rewards benefits, and helping them set up their mobile wallet are a few ways you can help members embrace the predominantly debit card-driven economy we now live in. Beyond these benefits, highlighting that your credit union is a single point of contact for questions, concerns, or in the event of any fraudulent activity can provided added peace of mind. Synergent’s Direct Marketing Services division helps support credit unions in educating members by providing newsletter articles and marketing materials.

Mobile vs. Physical Wallets: Demographic Disparity

Not everyone has taken the mobile wallet plunge just yet. While there are always some early adopters across demographics, spending preferences and habits vary wildly between generations. According to the J.D. Power 2016 U.S. Credit Card Satisfaction Study, the “emerging affluent are early adopters,” which are defined as members under 40 with annual incomes of $80,000 or more. Within this demographic, 43% of cardholders use a mobile payment app, compared to just 13% of consumers overall. Millennials (a group who roughly falls between the ages of 18 and 36) are most likely to have made a digital payment in the past 30 days, compared to their older counterparts.

There are a few top features that users of mobile wallets are seeking:

- Easy to use

- Faster checkout process

- Simple to set up

- Secure

- Wide acceptance

- Storage of loyalty rewards

Members are looking for a streamlined experience from the moment they load their cards into a mobile wallet or an app such as Amazon or PayPal. Once it is set up, the default card entered is likely to be used more than any other.

Making Space in the Marketplace

The Moebs Payment Study reflects that, in the next three to five years, debit and credit cards, ACH, and prepaid cards will continue to increase in usage, accounting for over 80% of all transactions. Technology is allowing for further expanded payment methods, such as Venmo and LevelUp for person to person (P2P) transactions. Because of these new methods, less cash is available in the marketplace. Credit unions may want to consider creating their own apps for payment to compete with this new competition and stay ahead of the curve.

“P2P payments are increasing in popularity amongst consumers based on several factors including the ability to move funds quickly from person to person,” stated Higgins. “Research is currently be conducted to determine how credit unions can position themselves to offer services that are similar to or better than what is being offered by large service providers such as Apple and Venmo. Zelle is a service that is of particular interest based on the ability to process real-time payments with the added fraud prevention services offered by Zelle’s owner, Early Warning Services (EWS).”